A settlement or judgement in a divorce does not absolve your client of liability on a defaulted SBA loan. Don't leave your client on the hook.

Book a Consultation CallThe common situation exists where a husband and wife co-own a business and obtain an SBA backed loan. Both parties sign a personal guarantee. Some time later the marriage fails and the parties split. However, as part of a settlement or judgement, one party takes over the business and remains responsible for the SBA loan.

The common mistake is assuming that because the marital settlement or divorce judgement states that one party is responsible for the SBA loan that the other spouse is absolved from liability. However, unless you have obtained a release from the personal guarantee, the personal guarantee remains in effect as to your client.

More importantly, the federal government does not care what the settlement or judgement says. Your client can seek indemnity form his or her former spouse as far as the SBA cares. This means, for example, if your client and his or her spouse obtained a $500,000 SBA loan, and your client's ex-spouse thereafter takes over the business and responsibility for the loan and defaults - your client remains on the hook for the $500,000 loan because he or she signed a personal guarantee.

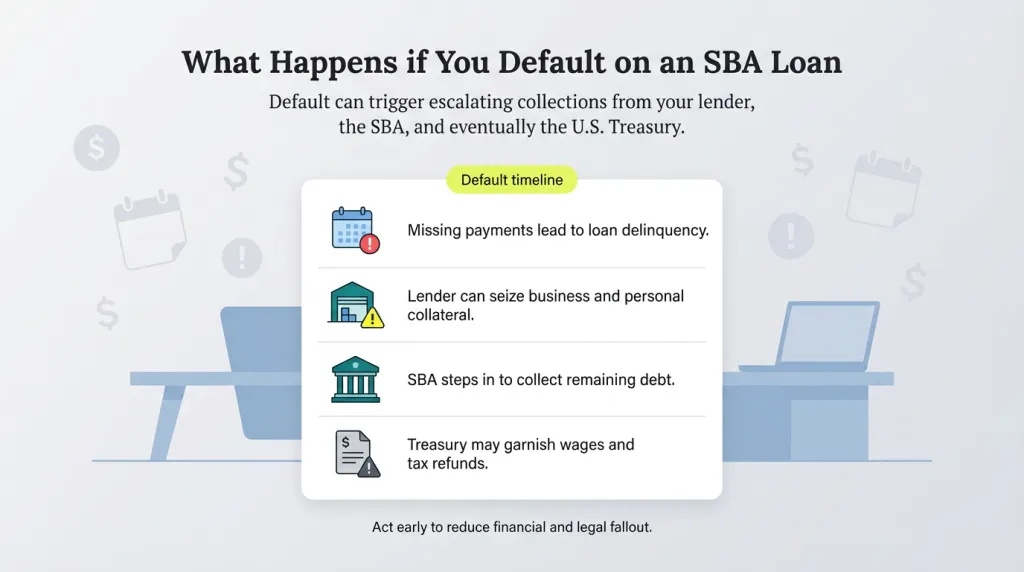

Your client can either pay the debt or risk submission to collection actions by the federal government. Collection can include a myriad of tools including filing a law suit, foreclosure, administrative wage garnishment, federal benefit or salary offset and tax refund offset. Your client may seek indemnity from his or her ex-spouse as a remedy, but while that process proceeds ... the government commences collection.

Protect Law Group provides assertive representation of clients fighting the SBA and collection by the federal government. Your client may settle his or her SBA debt with experienced legal representation. Better yet, move in front of the problem and contact Protect Law Group to help release your client from the personal guarantee.

Click here to download your free white paper from Protect Law Group:

Please contact us for a consultation at: 1-888-756-9969.

Millions of Dollars in SBA Debts Resolved via Offer in Compromise and Negotiated Repayment Agreements without our Clients filing for Bankruptcy or Facing Home Foreclosure

Millions of Dollars in Treasury Debts Defended Against via AWG Hearings, Treasury Offset Program Resolution, Cross-servicing Disputes, Private Collection Agency Representation, Compromise Offers and Negotiated Repayment Agreements

Our Attorneys are Authorized by the Agency Practice Act to Represent Federal Debtors Nationwide before the SBA, The SBA Office of Hearings and Appeals, the Treasury Department, and the Bureau of Fiscal Service.

Small business sole proprietor obtained an SBA COVID-EIDL loan for $500,000. Client defaulted causing SBA to charge-off the loan, accelerate the balance and refer the debt to Treasury's Bureau of Fiscal Service for aggressive collection. Treasury added $180,000 in collection fees totaling $680,000+. Client tried to negotiate with Treasury but was only offered a 3-year or 10-year repayment plan. Client hired the Firm to represent before the SBA, Treasury and a Private Collection Agency. After securing government records through discovery and reviewing them, we filed an Appeals Petition with the SBA Office of Hearings & Appeals (OHA) court challenging the SBA's referral of the debt to Treasury citing a host of purported violations. The Firm was able to negotiate a reinstatement and recall of the loan back to the SBA, participation in the Hardship Accommodation Plan, termination of Treasury's enforced collection and removal of the statutory collection fees.

Client personally guaranteed SBA 7(a) loan for $150,000. COVID-19 caused the business to fail, and the loan went into default with a balance of $133,000. Client initially hired a non-attorney consultant to negotiate an OIC. The SBA summarily rejected the ineligible OIC and the debt was referred to Treasury’s ureau of Fiscal Service for enforced collection in the debt amount of $195,000. We were hired to intervene and initiated discovery for SBA and Fiscal Service records. We were able to recall the case from Fiscal Service back to the SBA. We then negotiated a structured workout with favorable terms that saves the client approximately $198,000 over the agreed-upon workout term by waiving contractual and statutory administrative fees, collection costs, penalties, and interest.

Clients personally guaranteed SBA 504 loan balance of $750,000. Clients also pledged the business’s equipment/inventory and their home as additional collateral. Clients had agreed to a voluntary sale of their home to pay down the balance. We intervened and rejected the proposed home sale. Instead, we negotiated an acceptable term repayment agreement and release of lien on the home.

.jpg)