Aggressive SBA Debt Collection Is Happening in 2026: What Borrowers and Guarantors Must Know and Do Now

Aggressive SBA Debt Collection Is Happening in 2026. Learn what to expect and how Protect Law Group can help with SBA Debt Collection

We Provide Nationwide Representation of Small Business Owners, Personal Guarantors, and Federal Debtors with More Than $30,000 in Debt before the SBA and Treasury Department's Bureau of Fiscal Service

No Affiliation or Endorsement by any Federal Agency

An SBA Loan Modification is a remedial option when the business is still a viable concern, is still generating revenue and due to current circumstances, the old loan terms just do not make financial sense for all parties. A loan modification package is generally presented when it involves a SBA 504 Loan and the collateral or building’s fair market value has decreased significantly such that the loan should probably be modified (i.e. principal and interest payment terms, modification of principal loan balance to reflect current fair market value appraisal of real estate collateral, payment schedule etc.). In this situation, special factors need to be evaluated, appraisals will need to be conducted, and a proposal should be made in order to apply for a loan modification which benefits both parties. Again, the borrower will be required to provide updated business and personal financial information, additional pledged collateral may be requested, and appraisals will be done as part of the modification process. This is not a situation where the borrower or guarantor should engage in this process without qualified representation or consultation. However, if the business feels that it doesn’t need assistance, we recommend that you review applicable SBA SOPs and the Code of Federal Regulations (CFRs) prior to presenting your loan modification application.

The new Chapter 11 Subchapter V bankruptcy has many differences from a regular Chapter 11. For instance, some of the changes are as follows:

These changes will result in faster and thus less expensive reorganizations for small business.

The SBA can compromise a debt (that is, it can accept less than the full amount owed on a debt) based on the authority contained in the following statutes and regulatory sources:a. Section 5(b) of the Small Business Act which gives the Administrator authority to effect compromise settlements.b. The Federal Claims Collection Act (31 U.S.C. 3701 and following) which provides a means for the settlement, adjustment, and compromise of claims by Federal agencies.c. 4 CFR § 183, which prescribes standards for the compromise of claims under the Federal Claims Collection Act.

An SBA Offer in Compromise is not possible if the liability of the debtor is clear and the SBA can collect fully without protracted litigation. The amount offered for settlement must bear a reasonable relationship to the estimated value of the projected amount of recovery available through enforced collection. An SBA OIC is not available when the obligor has the ability to pay the deficiency in full within a reasonable time frame – generally, no later than 5 years. An OIC cannot be accepted if there is any evidence or knowledge of fraud, substantial misrepresentation, or financial dishonesty on the part of the offeror.

Creditors' committees commonly occur in traditional Chapter 11 cases, but they need a cause in Subchapter V cases.

Subchapter V trustees' primary function is to create a standard plan with the debtor and creditor. They do have the authority to audit the debtor's finances, but their primary purpose is mediation.

The reason for this is Congress sees impartial third-parties' increasing the likelihood of a sound resolution among the debtor and its creditors. Unbiased third parties are especially useful for small businesses whose creditors are tentative as a result of COVID.

Subchapter V allows debtors to spread their unsecured debt over 3 to 5 years. During this time, the debtor must devote their disposable income toward the debt. This model usually aids both parties involved.

The debtors have time to pay their debts and can spread them across a more extended period to avoid large sums. The creditors benefit because there is less a chance of debtors defaulting on longer-term payments.

Administrative expenses differ from Subchapter V to Chapter 11 cases. Debtors must pay administrative costs at plan confirmation in Traditional Chapter 11 cases. Debtors can pay Subchapter V administrative expenses over the life of the plan.

For both, however, debts are not discharged until the debtor completes all of its planned payments.

A charge off is justified when the SBA has complied with all requirements of collection and liquidation and further collection of any substantial portion of the debt is doubtful. The determination to justify a charge off may be based on one or more of the following:a) All efforts must have been exhausted in cost-effective recovery from:1. Voluntary payments from the borrower;2. Liquidation of collateral;3. Compromise with obligor leaving only a deficiency balance; and4. Consideration has been given to any legal remedies available so that no further reasonable expectation of recovery remains.b) Estimated costs of future collection exceed any anticipated recovery;c) Obligor cannot be located or is judgment proof;d) The Lender/SBA’s rights have expired (e.g., statute of limitations, restrictions of State law, SBA policy);e) Debt is legally without merit;f) Adjudication of a Chapter 7 Bankruptcy as a no asset case, or completion of Chap 11/13 case;g) The inability of the Lender to effect further worthwhile recovery.

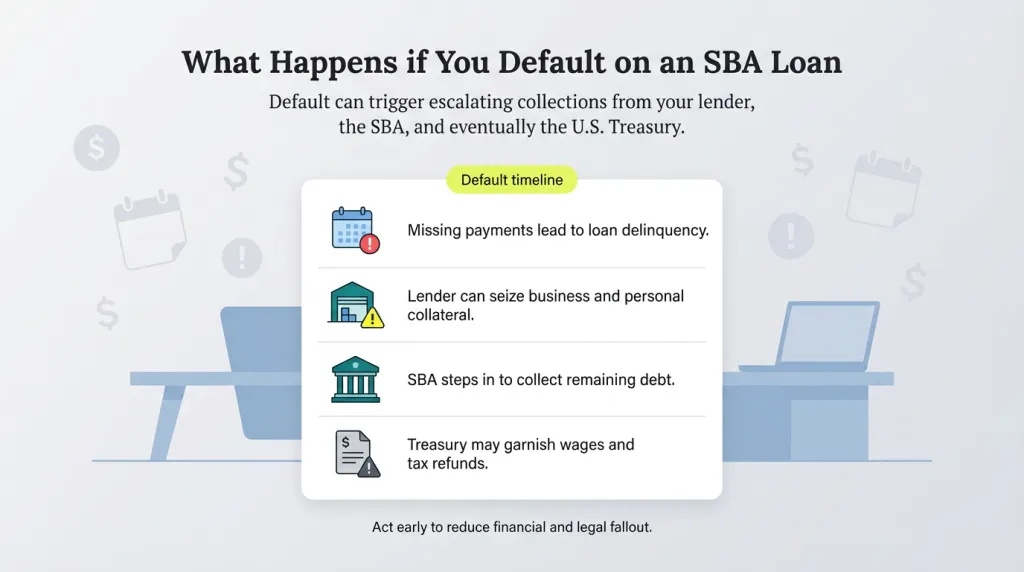

When you fail to make payments on your SBA loan, the bank or CDC will start contacting you asking for payment. Eventually, if non-payment continues, and you fail to cure the “default”, the bank or CDC may seek to collect on its collateral. This could include monies contained in an account housed at the same bank, your account receivables, your business equipment, real estate, even your home if you used a mortgage beyond the homestead exemption limits. You can expect that the bank or CDC will aggressively seize pledged collateral because the SBA requires the lender or CDC to take all appropriate steps to collect as much of the debt as it can before tendering a claim to the SBA for the balance. And if the United States Department of Treasury receives your account, then you can expect more aggressive collection action, and possibly, full-fledged litigation.

An SBA loan is a small business loan made by a private sector lender (such as a local bank or other lender) which is guaranteed by the United States Small Business Administration (“SBA”) pursuant to the terms of the U.S. Small Business Act, as amended (“Act”).

To be eligible for this option, a debtor must meet the following criteria:

The CARES Act further expanded the eligibility for businesses to qualify under this bankruptcy path.

This legislation increases the eligibility pool to also include companies with up to $7,500,000 in debt (both secured and unsecured) to reorganize under Subchapter V. This is a significant increase from the otherwise limit of $2,725,625.

When certain limited circumstances occur and a Borrower or Guarantor does not have the ability to make full payment, the SBA may allow a settlement for less than the full principal amount due on the federal debt. An SBA Offer in Compromise (OIC) is not possible without the cooperation of responsible Borrowers and Guarantors. One of the basic elements of an SBA OIC is that the business has ceased operations and all business assets have been liquidated. The business owner’s assistance and help in maximizing the recovery on the business assets will help to minimize the amount of deficiency balance on the loan. As in most scenarios involving debt forgiveness, there may be tax implications and small business owners should consult their tax and legal advisors before starting the SBA OIC process.

What Is The SBA Office Of Hearings And Appeals (OHA) And What Is Their Jurisdictional Power? CollapseThe Office of Hearings and Appeals (OHA) is an independent office of the Small Business Administration (SBA) established in 1983 to provide an independent, quasi-judicial appeal of certain SBA program decisions. The SBA OHA has authority to conduct proceedings in the following cases: Collection of debts owed to SBA and the United States under the Debt Collection Act of 1982, the Debt Collection Improvement Act of 1996, and part 140 of the aforesaid chapter; (t) Any other hearing, determination, or appeal proceeding referred to OHA by the Administrator of SBA, either through an SOP, Directive, Procedural Notice, or individual request by the Administrator to the SBA/OHA. The SBA OHA’s office is on the eighth floor of SBA headquarters above the Federal Center SW metro stop. Their office address is: 409 Third Street, SW, Eighth FloorWashington, DC 20416

The adequacy of an SBA OIC must begin with an evaluation of the assets of the obligor(s). The starting point is ordinarily the net present value of the forced sale value of such assets (not the loan balance). This value combined with the prognosis of the obligors’ earning power form the basis for determining the adequacy of the offer. The review must balance the right of the Government to collect the amount owed and the obligation to treat all obligors with dignity and fairness.

Each individual SBA OIC will be based on a case by case review of the Borrower’s or Guarantor’s individual financial situation and certain “litigative risks.” Factors that will be considered are:• An assessment of the debtor’s ability to pay and potential earnings capacity• Health and life expectancy• Local economic conditions• Equity in pledged or reachable assets• Settlement arrangements with other creditors• Applicable exemptions available to debtor under State and Federal law• The cost, time and risk of collection litigation

Yes, as long as you meet the criteria above individuals may avail themselves of Subchapter V.

A compromise with one or more Obligors does not release the continuing liability of any remaining Obligors. Each entity or individual responsible for the debt must develop its/his/her own SBA OIC.

An SBA Offer in Compromise with a “going concern” business is extremely rare and generally the SBA does will not consider this unless settlement arrangements have been made with all other creditors and the business must show it will not be able to operate under its current debt structure.

The following is a general list of categories that the SBA refers to in assessing the obligor’s ability to pay:a. Forced sale equivalent (liquidation value).(1) The basis for this value is normally the amount recoverable from the sale of the assets within a limited period of time (auction type sale). Also to be considered, is the time and expense needed for the SBA to gain control of the asset. But generally speaking, the SBA considers the following assets: Real Property (Commercial), (Residential), (Unimproved Land); Business Assets: (Machinery/Equipment), (Accounts Receivable/Inventory), (Furniture/Fixtures), (Leasehold Improvements).(2) The Claims Collection Act and the GAO standard provide that consideration be given to the time and monies involved with enforced collection to establish a discounted forced sales figure. The forced sale equivalent value needs to be adjusted for the following types of expenses: Court costs, filing fees; (a) Prior liens, taxes, assessments; (b) Costs of sale (auctioneer’s fees, advertising, lotting, and clean up costs); (c) Time of SBA employees (financial, legal, clerical, and administrative); (d) U.S. Attorney costs (professional, administrative, out of pocket); (e) Possibility of protested litigation or of bankruptcy and related expenses; (f) Time mandated by State redemption periods and the cost (depreciation, vandalism, insurance risks) that may result from such delays; (g) Care and protection expenses pending resale; (h) Extraordinary expenses of eviction, repairs to property, vandalism; (i) Costs necessary to bring property to marketable condition; (j) Transportation/travel costs; and (k) Discount reflecting the present value of future net recovery.b. Non-reachable assets and income.There may be items which are utilizable to the obligor(s) and have substantial value but are beyond the reach of the Government. The facts of the situation should enter into the Agency’s assessment of the obligor’s good faith.c. Jointly owned property.Special problems are encountered when the obligor shares ownership with another of an asset. This, by itself, is not sufficient reason to disregard the asset as having no value. The situation must be closely examined to determine (even to the extent of hiring appraisers and consultants) if the potential value of the property warrants further action.d. Individual asset valuations.Each worthwhile asset owned by the obligor needs to be assessed. Estimating the values of these assets is not an exact science but the SBA utilizes a uniformity of approach.(1) Cash.The SBA will only be concerned with cash in amounts substantially in excess of basic living expenses as determined from the SBA 770. Special accounts (IRA’s, Keoghs, trust accounts) should be valued net of early withdrawal penalties and other costs.(2) Cash surrender value (CSV) of life insurance.The SBA will determine the net amount receivable under the terms of the policy. Loans outstanding and other costs may also have to be subtracted out. The policy must often be surrendered in order to receive the CSV. The loan value should be used for analysis if surrendering the policy would leave the family with inadequate protection. This approach is to be used even if the Agency is acknowledged as assignee in the insurance company’s home office.(3) Accounts/notes receivable.The size, age, and collectibility of these assets will be examined to determine their worth. Typically they have little forced sale value. Ordinarily, the SBA will consider only large receivables with such attention.(4) Furniture, fixtures, and other personal effects.The SBA’s policy regarding this class of assets is that they are normally not worth very much. Efforts spent in other areas will yield much better results. The SBA will assign a nominal value to the contents of a modest home for compromise situations. If such assets are subject to an SBA lien, the lien may be realized for nominal value or the assets may be abandoned if no such release is possible.(5) Jewelry, paintings, antiques, and collections.When items in these categories have been assigned substantial value, the SBA will give them special attention. Outside sources may have to be utilized to determine meaningful values on these specialty items.(6) Automobiles.Automobiles generally have a ready market and various published books give a handy reference as to value. Gross compromise value “rule of thumb” is 80 percent of loan value. Of course prior encumbrances must be deducted to determine the net compromise value.(7) Securities.The SBA generally views the value of stocks and bonds in publicly traded firms as easily ascertainable and can quickly be converted to cash. Ownership interest in firms with closely held corporate stock and in unincorporated firms present much greater valuation problems. Each situation is considered using the best judgment available. If substantial potential worth is apparent, the SBA will obtain a valuation analysis by a chartered financial analyst or some other qualified person.(8) Other assets.Common carrier rights, copyrights, liquor licenses, patents, inheritances, and trusts are the types of assets that can be worthless or have substantial value. The SBA will confer with counsel regarding local laws and their effect on these assets. The establishment of values for these assets must rely on a reasonable assessment of the circumstances in each case.(9) Real estate.This is often the asset having the largest value on an SBA obligor’s or debtor’s balance sheet. For income producing or commercial properties, the SBA will use a member of a nationally recognized appraisal organization to conduct valuation analysis.(a) For the average residence, the SBA will consider some of the following acceptable alternatives:i. A “Property Report” by a recognized reporting service;ii. A written evaluation from a local realtor (with Multiple Listing Service (MLS) comparables);iii. A report from a residential appraiser used by Farmers Home Administration (FHA), Veterans Administration (VA), or other established mortgage lender; oriv. Any other local source you may have of similar reliability.(b) These reports usually furnish the market value of the property. However, this is not sufficient for SBA valuation purposes. The following must also be weighed:i. State redemption periods, homestead exemptions, and the like.These can substantially delay or negate the SBA’s ability to get the property: SBA will have to consult with counsel if there are any questions on the impact of this type of legislation. The value analysis must consider the recovery impact of local laws.ii. Policy regarding primary residence.Both the Department of Justice (DoJ) and SBA have strong positions regarding foreclosing on homes. For the SBA, a foreclosure action is generally considered as a very last resort. Concerted settlement efforts are generally first attempted, and fully documented in the loan file. Similarly, the DoJ will not, as a matter of policy, proceed with a foreclosure action if a reasonable settlement is at all possible or if the result will cause a cooperative debtor a severe hardship. This policy is consistent with the Claims Collection Act which says that a compromise settlement must be attempted before steps are taken to deprive obligors of their residences.

Subchapter V debtors must file their reorganization plan within 90 days of entering bankruptcy.

If the debtor cannot commit to a reorganization plan within 90 days, the debtor may file an extension plea. The bankruptcy court decides on whether to approve or deny the extension plea.

Approval of the plan will depend on whether any creditors object and the court's own calendar.

Chapter 11 of the US bankruptcy code focuses on “reorganizing” a business. This allows it to stay alive while restructuring debt and making a plan to repay creditors over time.

For many struggling businesses, the Chapter 11 Subchapter V is a long-awaited life preserver. A traditional Chapter 11 was extremely expensive for businesses. Businesses hope it eliminates some of the bureaucratic pitfalls of The Bankruptcy Abuse Prevention and Consumer Protection Act of 2005 (BAPCPA).

The BAPCPA was supposed to make filing for Chapter 11 easier. Instead, it included more reporting requirements and other burdens that bogged down the act and canceled out the benefits.

Subchapter V shares some similarities to the BAPCPA. Both have one-step confirmation, and both add new features that make filing for Chapter 11 easier for small businesses.

An SBA Offer in Compromise is generally on out-of-court work out option for a business which probably needs to shut down and there is no reasonable turnaround plan that can be executed to resurrect it from its current financial quandary. Furthermore, this remedial option is best utilized when it is apparent that the business’s pledged collateral is insufficient to pay off the outstanding loan balance and the personal guarantees of the owners are at stake.

While the SBA prefers a cash settlement offer (i.e., lump sum payment or cash compromise) with an SBA OIC Package, a monthly installment payment plan not to exceed 5 years or 60 months (term compromise) may also be considered if necessary. If a term compromise is desired, the SBA may also require a lien on any worthwhile collateral that may be available to secure the agreed upon balance due.

SOP 50 51 2A, Ch. 17, 8-12 states that “[a]ny settlement amount must bear a reasonable relationship to the present value of the estimated amount of recovery available through foreclosure (using a forced sale equivalent value) and enforced collection. This value, combined with the earning potential of the debtor, will form the basis for the offer in compromise.“ Litigative risks” involve answering certain legal questions as to the actual liability of the debtor and will be thoroughly explored by the SBA, if raised properly. The degree of doubt coupled with the potential costs, expenses and time involved in pursuing collection matters will generally determine the acceptable amount for a settlement. Thus, when considering an SBA OIC, it is very important for your qualified representative (who should have a background in litigation and thus be an attorney and have a working knowledge of SBA matters) to be able to advise SBA debtors regarding litigative risks and the costs associated with litigation and how all of these factors can impact the proposed offer to the Federal Government.

If your SBA loan is in default and you are working with your lender to wind down the business and settle the deficiency with an offer in compromise, time is of the essence. Banks generally do not wait much longer than 60-90 days after the defaulted borrower (business) has been liquidated or shut down to tender an OIC to the SBA for consideration which, if accepted, could potentially release the guarantors from the deficiency for a lesser amount. Generally speaking, the bank or CDC will send you what is commonly known as a Notice of Default, Acceleration and Demand for Payment for the entire loan balance due. If litigation is not a fiscally viable option and after certain collateral liquidation, you may be offered the chance to submit an SBA OIC with the bank or CDC for SBA consideration. If your case is ultimately transferred to the SBA, you should receive a 60-day Official Notice and demand for payment. If you fail to timely submit an SBA OIC within the administrative time frame as noted in this letter, the SBA will then refer your debt to the U.S. Department of Treasury for enforced collection, and thus, you will probably lose your one (1) time shot to settle for less than what is purportedly owed on the SBA debt through the SBA Offer in Compromise process..It should be noted that Treasury rarely collects on these bad loans directly – rather they hire private collection agencies (PCAs) to handle this. These PCAs don’t know anything about the history behind the loan – their job is to be ruthless in their collection endeavors as they generally receive a generous percent of the collected amount or actually bought the so-called junk federal debt for pennies on the dollar. Several of these federally approved private collection agencies or junk debt buyers are particularly nasty, and rarely settle for less than 50% of the outstanding amount as the incentives for collection, litigation and judgment pursuit are very high. Contrast that with the results that we have reviewed and settled and it’s easy to see the importance of addressing your outstanding SBA debt sooner rather than later, whether you’re working with a non-attorney consultant, an SBA Attorney or Federal Agency Practitioner, or attempting to do it yourself. If you think your banker is nasty or difficult to work with, you don’t want to experience the tactics of these collection agencies or junk debt buyers.

Most SBA loans fall under two categories: 7(a) and 504.In an SBA 7(a) transaction, a loan is secured from a private sector lender and, provided that the lender and borrower have satisfied the requirements of the SBA, if the borrower defaults on the loan, the SBA will reimburse the lender for a percentage on the loan loss (usually 75% or 85%, depending on various factors).In an SBA 504 transaction, typically, a loan is secured from a private sector lender with a first position lien covering up to 50% of the project cost, and a second loan is secured from a private sector lender with a junior lien position covering up to 40% of the project cost, and the borrower makes a contribution of equity equal to at least 10% of the project cost. After the closing of the first and second loans, and provided that the lender and borrower have complied with the requirements of the SBA, a debenture is sold to investors, the proceeds of which pays off the second loan, whereupon the second loan is assigned to a Certified Development Company (“CDC”) and then to the SBA, which provides a 100% guarantee of the debenture.The existence of the SBA’s guarantee in each of these transactions is an inducement for the lender to make a loan on terms it would otherwise not make. However, the SBA guarantee does not allow the lender to disregard standard commercial underwriting principles such as collateral and personal guarantees. The SBA guarantee does allow the lender to loan more money, extend longer terms, and approve loans to less mature businesses than it otherwise would.The SBA’s purpose under these financing programs is to help businesses gain more access to capital, thereby creating jobs and expanding the tax base. Pursuant to the Small Business Jobs Act of 2010 (“2010 Act”), the maximum SBA guarantee to the lender on a 7(a) loan was increased to $5,000,000; and on a 504 Loan, the maximum debenture amount was increased to $5,000,000.

If the principal debtor used his/her primary residence as security for a loan to fund the small business, there are available loan modifications.

If as part of your SBA loan, you pledged your primary residence as collateral, neither Chapter 7 or Chapter 13 bankruptcy will likely help in the event of default. However, Chapter 11 Subchapter V may help.

For instance, a small business debtor's plan may modify the rights of a holder of a claim secured by the principal residence of the debtor if the new value received in connection with the granting of the security interest was:

Therefore, you could possibly use the Chapter 11 Subchapter V to save your house and modify the terms of repaying the loan if you pledged your house as collateral as part of your personal guarantee. You will, more than likely, not rid yourself of the lien. Preserving your home constitutes your goal with the new bankruptcy code. If you have no other options, you should explore the new bankruptcy option.

Charge off is the process by which the SBA recognizes a loss and removes the uncollectible loan account from its active receivable accounts. The SBA’s policy is to be diligent and thorough in collection of federal debt and to promptly charge off all uncollectible accounts to more accurately reflect the status of the individual account and the Agency’s entire portfolio. It should be noted that a charge off is merely an administrative determination that does NOT affect SBA’s rights against any obligor nor reduce the SBA’s (or a participant lender’s) ability to proceed with any available remedy.

Filing fees with the court may vary but as of the time of this writing the filing fees are $1,738.

Attorneys' fees will vary on the complexity of your case but will be in the $15,000 to $25,000 range in most cases.

Under a regular Chapter 11, attorneys' fees were usually a minimum of $50,000.

If a Borrower or Obligor does not respond to the opportunity to submit an Offer in Compromise, they may be referred to the U.S. Department of Treasury for various enforced collection activities.

To determine if an SBA OIC is possible the following information must be provided;• A completed and signed SBA Form 1150 Offer in Compromise which outlines the terms of the offer and why the offer is being made. Be sure to address all the items on the forms “Instructions for Presenting the Offer” and “Elements of a Workable Compromise Offer.” You should also discuss the settlement arrangements that are being made with other creditors.• All offeror(s) must complete and sign an SBA Form 770 Financial Statement of Debtor and provide copies of the most recent two years of personal IRS Tax returns (or a copy of the Extension if not filed). The SBA Form 770 will be reviewed and compared with the original SBA Form 413 “Personal Financial Statement” completed at the time of loan approval. Valuations of property subject to judgment must be supported.• Copy of a current paystub if you are employed.• Additional information may be necessary depending on the individual circumstances of the transaction.

Even if your business incorporated (i.e. corporation, Limited Liability Company), almost all lenders and the SBA required that you sign personal guarantees as part of the initial loan funding process. Therefore, despite the fact that your business entity signed on the Loan Agreement with the bank or CDC, you would still be liable as a result of the personal guaranty that you or any other individuals signed. The personal guaranty, upon default on the loan, gives the bank or CDC and the SBA direct access to your personal assets such as your home, personal bank accounts, investments, real estate, etc.

Yes. The Agency Practice Act (5 U.S. Code Section 500 et seq.) specifically authorizes attorneys in good standing of the bar of the highest court of their State to represent you before the U.S. Small Business Administration, the U.S. Department of Treasury and the Bureau of Fiscal Service. However, if you decide to hire a non-attorney firm or consultant to handle your SBA matter before the aforesaid federal agencies, be advised that this non-attorney firm or consultant are in violation of the Federal Agency Practice Act, and cannot advise you on any legal issues. The problem we have with non-attorney representation for SBA matters in this industry is that we do not believe these non-attorneys have the legal authorization and ability to advise or counsel you on any interpretation of SBA administrative law (such as the SBA’s SOPs, the Code of Federal Regulations (CFRs), SBA OHA decisions, bankruptcy issues, federal/state statutory law or federal case law). In addition, many of these non-attorney representatives are neither affiliate members of NADCO, NAGGL (SBA trade associations) nor authorized to practice before the Department of Treasury pursuant to the Agency Practice Act and Circular 230. Finally, in the event that you need to appeal your case to the SBA Office of Hearings and Appeals in connection with your SBA debt or any adverse decision that may be considered an abuse of discretion, the non-attorney representatives will NOT be able to cite to legal precedent or argue applicable law before the SBA’s Administrative Law Judge (ALJ) as any attempt on their part would arguably be the unauthorized practice of law, and would be useless since these non-attorneys wouldn’t have any clue as to how to proceed with representing your interests in this special forum as these individuals do not have the education, training or experience to administratively litigate your case and protect your interests.

An SBA Guaranteed Loan with multiple personal guarantors considers each of the guarantors as being “jointly and severally” liable for the loan balance. This means that anyone who signed the loan as a borrower, obligor or a guarantor, is liable for the entire outstanding balance. Therefore, each and every guarantor can be pursued for the total loan balance. The problem that manifests with multiple guarantors after an SBA loan default is when certain individuals have more personal assets than others. Generally, lenders, the CDCs and the SBA target those personal guarantors who may have more assets than others. Hence, those individuals whose personal guarantees are “worthless” will generally not have to pay as much.

Under the Federal Statute of Limitations Act (28 U.S.C. 2415(a)), an action by the Government to recover upon a contract for money damages is barred unless filed within 6 years from the date the cause of action accrued. The date of the accrual of the cause of action may be subject to various interpretations. However, in the event of partial payment or written acknowledgement of the debt, the cause of action again accrues at the time of the partial payment or acknowledgement. 28 U.S.C.A. § 2415(a).

An SBA Loan Deferment is a temporary remedial option. If your business is having short term financial difficulty because of a seasonal slump and can reasonably prove through pro forma financial statements to your lender or CDC that a turnaround is around the corner and you need brief relief from paying on the SBA loan, you should consider applying for a deferment. Generally, if you qualify, your bank or CDC, with the SBA’s approval can provide you with either a six (6) month or twelve (12) month reprieve from paying either the principal amount (and allow interest-only payments) or no principal and interest. However, if you consider this option, be advised that you may be asked to reaffirm the loan with personal guarantees or even pledge additional collateral. Needless to say, this is not an option that you should consider without either representation or consultation with a qualified practitioner.

Small business sole proprietor obtained an SBA COVID-EIDL loan for $500,000. Client defaulted causing SBA to charge-off the loan, accelerate the balance and refer the debt to Treasury's Bureau of Fiscal Service for aggressive collection. Treasury added $180,000 in collection fees totaling $680,000+. Client tried to negotiate with Treasury but was only offered a 3-year or 10-year repayment plan. Client hired the Firm to represent before the SBA, Treasury and a Private Collection Agency. After securing government records through discovery and reviewing them, we filed an Appeals Petition with the SBA Office of Hearings & Appeals (OHA) court challenging the SBA's referral of the debt to Treasury citing a host of purported violations. The Firm was able to negotiate a reinstatement and recall of the loan back to the SBA, participation in the Hardship Accommodation Plan, termination of Treasury's enforced collection and removal of the statutory collection fees.

Client personally guaranteed SBA 7(a) loan balance of over $150,000. Business failed and eventually shut down. SBA then pursued client for the balance. We intervened and was able to present an SBA OIC that was accepted for $30,000.

Client personally guaranteed SBA 7(a) loan for $350,000. The small business failed but because of the personal guarantee liability, the client continued to pay the monthly principal & interest out-of-pocket draining his savings. The client hired a local attorney but quickly realized that he was not familiar with SBA-backed loans or their standard operating procedures. Our firm was subsequently hired after the client received the SBA's official 60-day notice. After back-and-forth negotiations, we were able to convince the SBA to reinstate the loan, retract the acceleration of the outstanding balance, modify the original terms, and approve a structured workout reducing the interest rate from 7.75% to 0% and extending the maturity date for a longer period to make the monthly payments affordable. In conclusion, not only we were able to help the client avoid litigation and bankruptcy, but our SBA lawyers also saved him approximately $227,945 over the term of the workout.

Millions of Dollars in SBA Debts Resolved via Offer in Compromise and Negotiated Repayment Agreements without our Clients filing for Bankruptcy or Facing Home Foreclosure

Millions of Dollars in Treasury Debts Defended Against via AWG Hearings, Treasury Offset Program Resolution, Cross-servicing Disputes, Private Collection Agency Representation, Compromise Offers and Negotiated Repayment Agreements

Our Attorneys are Authorized by the Agency Practice Act to Represent Federal Debtors Nationwide before the SBA, The SBA Office of Hearings and Appeals, the Treasury Department, and the Bureau of Fiscal Service.

.jpg)