Aggressive SBA Debt Collection Is Happening in 2026: What Borrowers and Guarantors Must Know and Do Now

Aggressive SBA Debt Collection Is Happening in 2026. Learn what to expect and how Protect Law Group can help with SBA Debt Collection

Are you straining with your SBA loan repayment and you are opting to defer the loan. Read this article to know how you can get an SBA loan deferment.

Book a Consultation CallAre you struggling to pay your SBA loan? Are you unsure about what to do next?

If you're facing this dilemma, you're not alone. Half of all small businesses struggle financially and often fold in the first five years.

But it doesn't have to be this way. A simple loan deferment could help you get back on track and save your business.

Here's what you need to know about an SBA loan deferment.

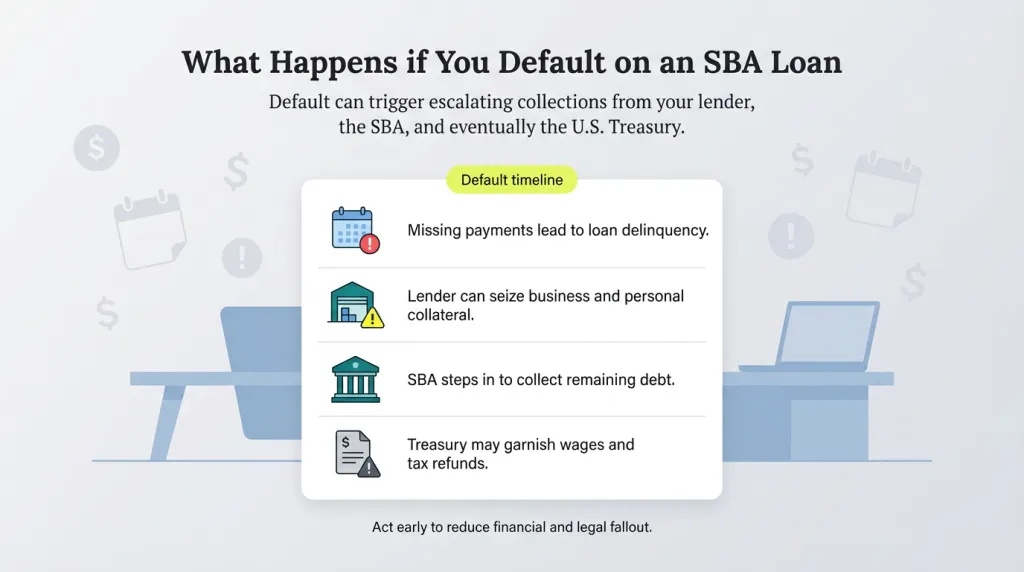

Accumulating too much debt early on can be a huge problem for a small business. Falling into debt you can't pay can lead to mountains of interest that only compounds the problem.

When you're on the verge of losing your business, it's scary. You may be tempted to file bankruptcy to end the debt and the worrying.

However, you should avoid bankruptcy if at all possible. Declaring bankruptcy often doesn't make sense for a small business and will make it hard to get any future business loans.

Before you choose bankruptcy, you should know there are debt relief options that can help you manage your debt and keep your business running.

The current pandemic has affected small business owners everywhere. Although some small businesses were able to rebound quickly, others have struggled.

Although private financial institutions provide SBA loans, they are backed by the Federal government through the SBA. This means SBA loans are secure loans that require collateral.

If you default, the lender has a right to recover what you owe. That could put your collateral, including your primary residence, business assets, car, etc. at risk.

Eliminating your small business debt is crucial for getting your business moving in the right direction. You need financial relief so you can focus on running your business.

An experienced SBA debt attorney understands the stress you may be dealing with right now. They know that eliminating your debt is the first step toward financial freedom.

An SBA attorney may be able to negotiate for a sizable reduction in your small business debt, including a reduction in principal. For many business owners, a more manageable debt makes all the difference.

With the right guidance, you may be able to avoid bankruptcy and eliminate or greatly reduce your debt.

The role of an SBA attorney is to help you restructure your business debt and get the relief you need so you can focus on running your business. It's important to have a professional guiding you through this process.

Many debt relief companies claim they can help you resolve your debt problems but are unable to fulfill this promise. Having an experienced SBA attorney working for you ensures you have the best chance for debt relief.

A skilled negotiator knows how to deal with creditors, work to protect your rights, and get the best deal possible for you. Your SBA attorney will keep all your financial dealings confidential.

This ensures that your financial issues will remain private and will not disrupt your company's reputation.

Your attorney will work with your creditors to negotiate a lesser debt on your behalf. Creditors are more likely to offer a better deal when you have an attorney representing you.

An SBA attorney is familiar with collection laws and what a creditor can and cannot do when attempting to collect a debt. They will communicate directly with your creditors and will instruct them to stop contacting you.

If you are facing an SBA loan default, don't settle for bankruptcy.

Instead, hire a reputable SBA attorney to help you with the process of SBA debt settlement.

Before any litigation occurs, it's possible to enter into settlement negotiations with your lender for a deferment or other workout of the loan. A deferment provides you with some breathing room and enables you to get your business on the right track before paying your monthly loan commitment.

The terms of a deferment can vary as will the "catch up" provisions.

Every case is different. It's in your best interest to have an SBA attorney by your side every step of the way.

When you're faced with an SBA loan default, the worst thing to do is bury your head in the sand. The sooner you begin seeking a loan deferment, the better.

The worst case scenario most often results in the lender filing a lawsuit.

For this reason, the sooner you address the problem and begin working with an SBA attorney, the better.

Don't wait until it's too late to save your business. Start the SBA loan deferment process right away.

The experienced legal team of Protect Law Group provides real solutions for individuals facing SBA loan problems. We're here to help. Contact us today for a case evaluation.

Millions of Dollars in SBA Debts Resolved via Offer in Compromise and Negotiated Repayment Agreements without our Clients filing for Bankruptcy or Facing Home Foreclosure

Millions of Dollars in Treasury Debts Defended Against via AWG Hearings, Treasury Offset Program Resolution, Cross-servicing Disputes, Private Collection Agency Representation, Compromise Offers and Negotiated Repayment Agreements

Our Attorneys are Authorized by the Agency Practice Act to Represent Federal Debtors Nationwide before the SBA, The SBA Office of Hearings and Appeals, the Treasury Department, and the Bureau of Fiscal Service.

Client personally guaranteed SBA 7(a) loan for $150,000. COVID-19 caused the business to fail, and the loan went into default with a balance of $133,000. Client initially hired a non-attorney consultant to negotiate an OIC. The SBA summarily rejected the ineligible OIC and the debt was referred to Treasury’s ureau of Fiscal Service for enforced collection in the debt amount of $195,000. We were hired to intervene and initiated discovery for SBA and Fiscal Service records. We were able to recall the case from Fiscal Service back to the SBA. We then negotiated a structured workout with favorable terms that saves the client approximately $198,000 over the agreed-upon workout term by waiving contractual and statutory administrative fees, collection costs, penalties, and interest.

Our firm successfully resolved an SBA COVID-19 Economic Injury Disaster Loan (EIDL) default in the amount of $150,000 on behalf of Illinois-based client. After the business permanently closed due to the economic impacts of the pandemic, the owners faced potential personal liability if the business collateral was not liquidated properly under the SBA Security Agreement.

We guided the client through the SBA’s Business Closure Review process, prepared a comprehensive financial submission, and negotiated directly with the SBA to release the collateral securing the loan. The borrower satisfied their collateral obligations with a payment of $2,075, resolving the SBA’s security interest.

Clients obtained an SBA 7(a) loan for their small business in the amount of $298,000. They pledged their primary residence and personal guarantees as direct collateral for the loan. The business failed, the lender was paid the 7(a) guaranty money and the debt was assigned to the SBA. Clients received the Official 60-Day Notice giving them a couple of options to resolve the debt balance directly with the SBA before referral to Treasury's Bureau of Fiscal Service. The risk of referral to Treasury would add nearly $95,000 to the SBA principal loan balance. With the default interest rate at 7.5%, the amount of money to pay toward interest was projected at $198,600. Clients hired the Firm with only 4 days left to respond to the 60-Day due process notice. Because the clients were not eligible for an Offer in Compromise (OIC) due to the significant equity in their home and the SBA lien encumbering it, the Firm Attorneys proposed a Structured Workout to resolve the SBA debt. After back and forth negotiations, the SBA Loan Specialist assigned to the case approved the Workout terms which prevented potential foreclosure of their home, but also saved the clients approximately $294,000 over the agreed-upon Workout term with a waiver of all contractual and statutory administrative fees, collection costs, penalties, and interest.

.jpg)