SBA Loan Default: 6 Things You Should Know

Are you concerned with what to do in the event of an SBA loan default? Then read about some things you'll need to consider when defaulting on an SBA loan.

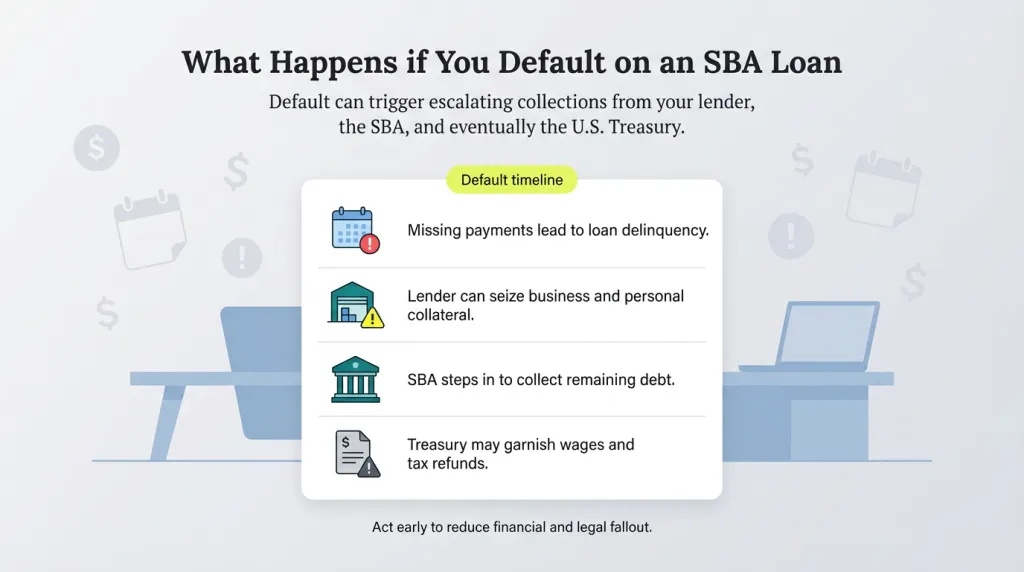

SBA has helped many business owners grow their business through providing funding when other lenders didn't. However, if you default on one of these types of SBA loans, you will be subject to administrative wage garnishment.

Administrative Wage Garnishment

Here are the types of SBA funding loans available to you:

These loans are the most common and known type of SBA funding. SBA 7(a) loans can be used to start a business, acquire an existing business, buying equipment and inventory, refinance existing debt, among others.

These loans offer up to $5 million in funding with a 10 to 25-year repayment. The interest rates range from 5.75% to 8.25%.

An up to 10-year repayment option applies for a working capital loan. For commercial real estate applies up to 20-year repayment option. SBA 7(a) loans may require a 10% to 20% down payment, and collateral.

SBA express loans follow the same guidelines that the SBA 7(a). But, the loan amounts for these are from $5,000 to $350,000. The interest rates on these loans range from 4.5% to 6.5% plus prime rate.

The loan terms for the SBA express loans are up to 7 years for a line of credit, up to 25 years for real estate, and from 5 to 10 years for other purposes. These loans can be used for additional working capital, cash flow, buy supplies and inventory, among others.

These loans help small businesses in disadvantaged markets to get access to funding. The amounts of SBA community advantage loans are up to $250,000 provided through community-based lenders. The interest rates on these loans are 6% plus prime rate.

The repayment terms on these loans range from up to 7 to 25 years. For working capital and startup expenses, range from up to 7 to 10 years. If the loan is for real estate, the repayment term will be for up to 25 years.

These loans are provided to startups and small businesses that don't have enough credit record to get approved for a traditional loan. These funds can be used for purchasing real estate, working capital or expanding your existing business.

SBA microloans are offered help small businesses, startups, and non-profit child-care centers with their working capital needs. These loans provide up to $50,000 in funding. These loans can be used as working capital, purchase inventory and supplies, startup capital, among others.

The interest rates on these loans range from 6.5% to 13%. The repayment term is a maximum of up to 6 years. These loans can't be used to purchase real estate or pay existing debts.

These loans are offered by the Certified Development Company (CDC) and SBA 504 program. CDC/SBA 504 loans are provided to small businesses for the construction, purchase or renovation of commercial real estate properties, and other fixed assets like equipment.

The loan amounts are up to $5.5 million. Depending on the purpose of the loan, the loan terms may be 10 or 20 years. The interest rates range from 4% to 8%.

The SBA CAPLine provides lines of credit to help small businesses their working capital needs. These may be used to cover the business's cash flow requirements, fulfilling purchase orders, renovation of commercial properties, among others.

The amounts of these lines of credit are up to $5 million, and up to $200,000 for small business asset based lines. The interest rates range from 5.75% to 8.25%. The repayment terms are for up to 5 years. You may have to provide collateral such as inventory, invoices, purchase orders, contracts, among others.

These loans are offered to small business exporters. These may help them enter new foreign markets, international transactions, and expand their exporting operations.

The amounts of these loans are from up to $500,000 and $5 million. Repayment terms on these loans are up to 3, 7, and 25 years. The 3 types of SBA export loans are SBA Export Express loans, SBA Export Working Capital loans, and SBA International Trade loans.

SBA disaster loans are offered businesses that have suffered damages or been destroyed by a declared disaster. These loans can be used as working capital, operating expenses, and to replace or repair assets like inventory, equipment, personal property, and real estate.

These loans can provide up to $2 million in funding. The interests range from 4% to 8%. Repayment terms are up to 30 years. The 3 types of SBA disaster loans are SBA Business Physical Disaster loans, SBA Economic Injury Disaster loans, and SBA Military Reservists Economic Injury loans.

If you have obtained any one of these SBA loans and have defaulted, the Department of Treasury can subject you to an administrative wage garnishment without obtaining a state court judgment first. This means the Department of Treasury can take up to 15% of each paycheck to pay down the debt.

The Debt Collection Improvement Act (DCIA) specifically states that the ability to garnish your wages through administrative wage garnishment applies notwithstanding any state law. The Supremacy Clause of the United States Constitution (Article VI, Clause 2) establishes that the Constitution, federal laws made pursuant to it, and treaties made under its authority, constitute the supreme law of the land. As such, federal law preempts state law if there is a conflict or if federal law specifically states that it preempts state law, as is the case with administrative wage garnishment. You are still entitled to due process, however, before an administrative wage garnishment can start. This means that the Department of Treasury must provide you with notice and a reasonable opportunity to be heard and present evidence in your favor before it can commence the administrative wage garnishment.

As stated in the article, you are entitled to a hearing before the Department of Treasury commences administrative wage garnishment. You have rights and you should have assertive legal representation to assert those rights. Contact us to learn more about our Administrative Wage Garnishment defense services.

Millions of Dollars in SBA Debts Resolved via Offer in Compromise and Negotiated Repayment Agreements without our Clients filing for Bankruptcy or Facing Home Foreclosure

Millions of Dollars in Treasury Debts Defended Against via AWG Hearings, Treasury Offset Program Resolution, Cross-servicing Disputes, Private Collection Agency Representation, Compromise Offers and Negotiated Repayment Agreements

Our Attorneys are Authorized by the Agency Practice Act to Represent Federal Debtors Nationwide before the SBA, The SBA Office of Hearings and Appeals, the Treasury Department, and the Bureau of Fiscal Service.

Client personally guaranteed an SBA 7(a) loan for $100,000 from the lender. The SBA loan went into early default in 2006 less than 12 months from disbursement. The SBA paid the 7(a) guaranty monies to the lender and subsequently acquired the deficiency balance of about $96,000, including the right to collect against the guarantor. However, the SBA sent the Official 60-Day Due Process Notice to the Client's defunct business address instead of his personal residence, which he never received. As a result, the debt was transferred to Treasury's Bureau of Fiscal Service where substantial collection fees were assessed, including accrued interest per the promissory note. Treasury eventually referred the debt to a Private Collection Agency (PCA) - Pioneer Credit Recovery, Inc. Pioneer sent a demand letter claiming a debt balance of almost $310,000 - a shocking 223% increase from the original loan amount assigned to the SBA. Client's social security disability benefits were seized through the Treasury Offset Program (TOP). Client hired the Firm to represent him as the debt continued to snowball despite seizure of his social security benefits and federal tax refunds as the involuntary payments were first applied to Treasury's collection fees, then to accrued interest with minimal allocation to the SBA principal balance.

We initially submitted a Cross-Servicing Dispute (CSD) challenging the referral of the debt to Treasury based on the defective notice sent to the defunct business address. Despite overwhelming evidence proving a violation of the Client's Due Process rights, the SBA still rejected the CSD. As a result, an Appeals Petition was filed with the SBA Office of Hearings & Appeals (OHA) Court challenging the SBA decision and its certification the debt was legally enforceable in the amount claimed. After several months of litigation before the SBA OHA Court, our Firm Attorney successfully negotiated an Offer in Compromise (OIC) Term Workout with the SBA Supervising Trial Attorney for $82,000 spread over a term of 74 months at a significantly reduced interest rate saving the Client an estimated $241,000 in Treasury collection fees, accrued interest (contract interest rate and Current Value of Funds Rate (CVFR)), and the PCA contingency fee.

Our firm successfully resolved an SBA COVID-19 Economic Injury Disaster Loan (EIDL) in the original amount of $150,000 for a Florida-based borrower. The loan, issued on June 4, 2020, was secured by business assets and potential personal liability through the SBA's Security Agreement.

Following the permanent closure of the business, we guided the client through the SBA’s Business Closure Review process and prepared a comprehensive collateral analysis. We negotiated directly with the SBA, obtaining a full release of the business collateral for $2,910 — satisfying the borrower’s obligations under the Security Agreement and eliminating any further enforcement risk against the pledged assets.

Client personally guaranteed SBA 7(a) loan for $350,000. The small business failed but because of the personal guarantee liability, the client continued to pay the monthly principal & interest out-of-pocket draining his savings. The client hired a local attorney but quickly realized that he was not familiar with SBA-backed loans or their standard operating procedures. Our firm was subsequently hired after the client received the SBA's official 60-day notice. After back-and-forth negotiations, we were able to convince the SBA to reinstate the loan, retract the acceleration of the outstanding balance, modify the original terms, and approve a structured workout reducing the interest rate from 7.75% to 0% and extending the maturity date for a longer period to make the monthly payments affordable. In conclusion, not only we were able to help the client avoid litigation and bankruptcy, but our SBA lawyers also saved him approximately $227,945 over the term of the workout.

.jpg)