Current SBA Guidelines on EIDL Loan Settlements

Struggling with a COVID EIDL loan? Learn how the SBA's Offer in Compromise works in 2025, eligibility rules, and settlement options before policies change.

Generally, there are at least seven (7) legal sources to consider reviewing in connection with trying to settle SBA debt, resolve SBA loan default or defend against a DOT collection matter. The seven (7) sources that we believe are essential for research into these important issues are:

When locating certain research sources to settle SBA debt case or defend against a DOT collection matter, we often break our initial research into two (2) parts:

Legal Research Sources Internal to the SBA:

Legal Research Sources External to the SBA:

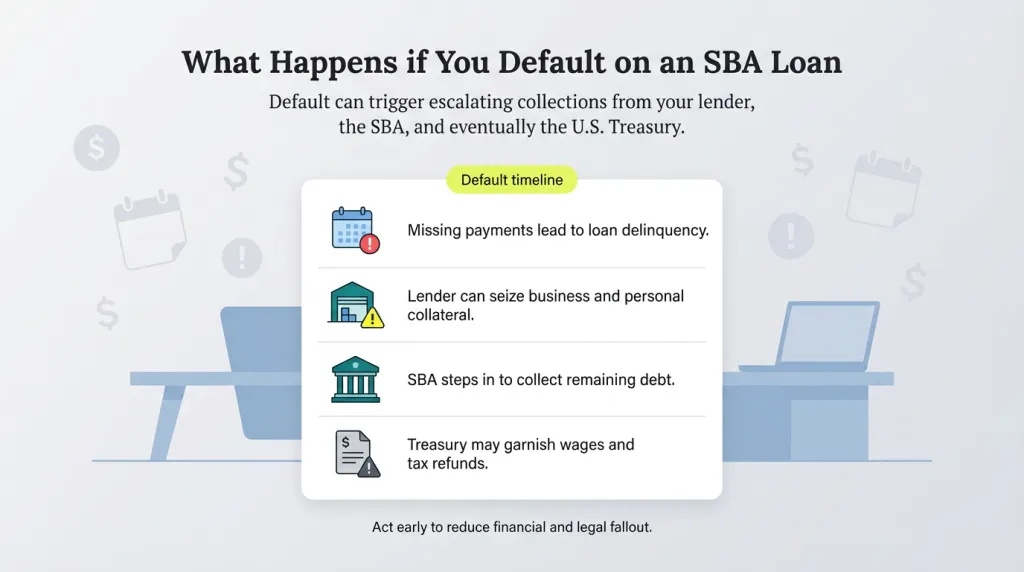

Hence, there are several branches of legal resources and authorities which need to be researched and reviewed when dealing with any SBA loan default, SBA OIC or DOT debt collection matter. To say that it is okay to simply ignore these important resources, then any SBA or DOT debtor told to do so, has been advised by the non-attorney salesperson who simply does not know what “he” is talking about, and in all reality . . . is providing not only irresponsible advice, but also negligent counsel. Typical . . . I guess for a “non-attorney” who neither has a doctorate, passed a bar exam (or multiple bar examinations), practiced law for several years (but is trying to do so in an arguably unauthorized and illegal fashion) nor worked with such important federal agency issues. Generally, when you don’t possess something . . . human nature tells you to criticize what you don’t possess. It’s nothing more than a “defense mechanism” in order to deal with a severe inferiority complex

You should not have to struggle to settle SBA debt on your own. Instead, turn to one of our attorneys who specializes in SBA OIC & DOT debt claims. We are dedicated to helping you settle SBA loan default and/or federal nontax debt with the DOT.

If you are struggling with circumstances that involve SBA loan default and/or a DOT referral, you deserve professional help! Our attorneys all know how to win SBA OIC and DOT compromise cases. If you contact us, we can help you settle SBA debt once and for all. After you schedule an appointment, you confer with a devoted SBA OIC lawyer and/or United States Treasury Dept. Practitioner who will help you through your administrative legal battle. After your claim is resolved, you will never again have to worry about your SBA loan default problem and/or DOT collection claim haunting you. Our team of lawyers has assisted many clients through the years. Now it is your turn! You truly can resolve SBA debt and/or DOT matter for good!

Millions of Dollars in SBA Debts Resolved via Offer in Compromise and Negotiated Repayment Agreements without our Clients filing for Bankruptcy or Facing Home Foreclosure

Millions of Dollars in Treasury Debts Defended Against via AWG Hearings, Treasury Offset Program Resolution, Cross-servicing Disputes, Private Collection Agency Representation, Compromise Offers and Negotiated Repayment Agreements

Our Attorneys are Authorized by the Agency Practice Act to Represent Federal Debtors Nationwide before the SBA, The SBA Office of Hearings and Appeals, the Treasury Department, and the Bureau of Fiscal Service.

Clients obtained an SBA 7(a) loan for $324,000 to buy a small business and its facility. The business and real estate had an appraisal value of $318,000 at the time of purchase. The business ultimately failed but the participating lender abandoned the business equipment and real estate collateral even though it had valid security liens. As a result, the lender recouped nearly nothing from the pledged collateral, leaving the business owners liable for the deficiency balance. The SBA paid the lender the 7(a) guaranty money and was assigned ownership of the debt, including the right to collect. However, the clients never received the SBA Official 60-Day Notice and were denied the opportunity to negotiate an Offer in Compromise (OIC) or a Workout directly with the SBA before being transferred to Treasury's Bureau of Fiscal Service, which added an additional $80,000 in collection fees. Treasury garnished and offset the clients' wages, federal salary and social security benefits. When the clients tried to negotiate with Treasury by themselves, they were offered an unaffordable repayment plan which would have caused severe financial hardship. Clients subsequently hired the Firm to litigate an Appeals Petition before the SBA Office & Hearings Appeals (OHA) challenging the legal enforceability and amount of the debt. The Firm successfully negotiated a term OIC that was approved by the SBA Office of General Counsel, saving the clients approximately $205,000.

Our firm successfully negotiated an SBA offer in compromise (SBA OIC), settling a $974,535.93 SBA loan balance for just $18,000. The offerors, personal guarantors on an SBA 7(a) loan, originally obtained financing to purchase a commercial building in Lancaster, California.

The borrower filed for bankruptcy, and the third-party lender (TPL) foreclosed on the property. Despite the loan default, the SBA pursued the offerors for repayment. Given their limited income, lack of significant assets, and approaching retirement, we presented a strong case demonstrating their financial hardship.

Through strategic negotiations, we secured a favorable SBA settlement, reducing the nearly $1 million debt to a fraction of the amount owed. This outcome allowed the offerors to resolve their liability without prolonged financial strain.

Our firm successfully resolved an SBA COVID-19 Economic Injury Disaster Loan (EIDL) default in the amount of $150,000 on behalf of Illinois-based client. After the business permanently closed due to the economic impacts of the pandemic, the owners faced potential personal liability if the business collateral was not liquidated properly under the SBA Security Agreement.

We guided the client through the SBA’s Business Closure Review process, prepared a comprehensive financial submission, and negotiated directly with the SBA to release the collateral securing the loan. The borrower satisfied their collateral obligations with a payment of $2,075, resolving the SBA’s security interest.

.jpg)