SBA Loan Acceleration: Understanding Notice and Your Legal Options

Explore SBA loan acceleration's impact. Learn triggers, implications, and legal options to defend against accelerated payment demands.

How the Federal Government Shutdown Affects SBA Loan Borrowers and Guarantors

Book a Consultation CallThe federal government shutdown that began on October 1, 2025, has significantly impacted small businesses nationwide as the U.S. Small Business Administration (SBA) suspended most of its core lending and contracting programs. According to the SBA’s contingency plan, nearly 23% of the agency’s workforce was furloughed. While 4,745 of 6,201 employees were retained, key divisions—including Capital Access, Field Operations, and the Office of General Counsel—experienced sharp reductions.

When headlines announce a federal government shutdown, small business owners and guarantors with SBA loans often ask: “Does this pause my payments or stop collections?” The short answer is no. A shutdown creates administrative delays, but it does not suspend your legal obligations as a borrower or guarantor. At Protect Law Group, we guide clients nationwide through these high-risk situations.

The U.S. Small Business Administration (SBA) relies on annual appropriations for most of its programs. During a lapse in funding:

The Bureau of the Fiscal Service (BFS), part of the U.S. Treasury, is responsible for government-wide debt collection. Its shutdown plan treats debt collection and the Treasury Offset Program (TOP) as “excepted” activities. That means federal loan debts referred to Treasury can still trigger:

Even while SBA is scaled back, Treasury’s enforcement mechanisms remain operational.

For borrowers and personal guarantors, a shutdown means:

If you are a borrower or guarantor:

Q: Do I still have to make my SBA loan payments during a shutdown?

Yes. A government shutdown does not suspend your repayment obligations. Interest and penalties continue to accrue even if SBA staff are furloughed.

Q: Can I apply for a new SBA loan during a shutdown?

No. New 7(a) and 504 loan applications are paused until Congress restores SBA funding. Even lenders with delegated authority cannot approve new loans during the lapse.

Q: What about disaster loans?

SBA disaster loans usually continue, since they are funded separately. However, you may face slower processing times.

Q: Can I request a loan modification, deferment, or reinstatement?

You can submit requests, but most require SBA review. These are considered “non-excepted” functions and will not be processed until the shutdown ends.

Q: Does the government stop collecting on SBA debts during a shutdown?

Not entirely. If your loan has been referred to the Treasury’s Bureau of the Fiscal Service, collections—including tax refund offsets, Social Security offsets, and cross-servicing—will continue.

Q: Will foreclosure or liquidation stop?

Not completely. The SBA can still approve limited liquidation or collateral protection actions if there is risk of “imminent loss” to government assets.

Q: Could the shutdown help me as a guarantor?

In limited ways. You may get a temporary reprieve from new enforcement or settlement negotiations. But once SBA reopens, expect a backlog-driven surge in activity, including possible acceleration of default cases.

Q: What should I do now if I’m behind on payments?

Led by former Georgia Senator (Republican) and the current SBA Administrator, Kelly Loeffler, the SBA website displays a bright red "Special Announcement" message that provides the following:

Senate Democrats voted to block a clean federal funding bill (H.R. 5371), leading to a government shutdown that is preventing the U.S. Small Business Administration (SBA) from serving America’s 36 million small businesses.

Every day that Senate Democrats continue to oppose a clean funding bill, they are stopping an estimated 320 small businesses from accessing $170 million in SBA-guaranteed funding.

As a result of the shutdown, we wanted to notify you that many of our services supporting small businesses are currently unavailable. The agency is executing its Lapse Plan and as soon as the shutdown is over, we are prepared to immediately return to the record-breaking services we were providing under the leadership of the Trump Administration.

If you need disaster assistance, please visit sba.gov/disaster.

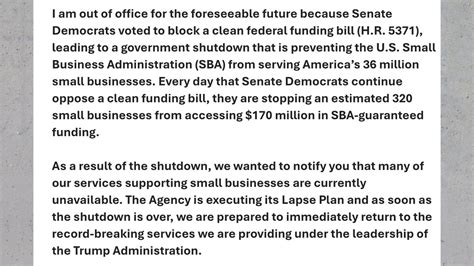

The automatic response emails from several furloughed SBA staffers state the following:

Below is the transcribed text from the furloughed SBA Staffer's email:

“I am out of office for the foreseeable future because Senate Democrats voted to block a clean federal funding bill (H.R. 5371), leading to a government shutdown that is preventing the U.S. Small Business Administration (SBA) from serving America’s 36 million small businesses.”

“Every day that Senate Democrats continue (to) oppose a clean funding bill, they are stopping an estimated 320 small businesses from accessing $170 million in SBA-guaranteed funding.”

“As a result of the shutdown, we wanted to notify you that many of our services supporting small businesses are currently unavailable. The Agency is executing its Lapse Plan and as soon as the shutdown is over, we are prepared to immediately return to the record-breaking services we are providing under the leadership of the Trump Administration.”

The government shutdown does not cancel SBA debt. It creates delays for new loans and discretionary relief, while Treasury’s collection authority remains live. At Protect Law Group, we help business owners and guarantors use this window strategically—preparing defenses and settlement packages so they are ready the moment SBA reopens.

Contact an experienced SBA loan defense attorney immediately.

Our SBA Attorneys have guided thousands of small businesses through reviews, contested or negotiated debts assessed against owners, officers and guarantors, and litigated cases at the SBA Office of Hearings & Appeals (OHA) Court before presiding Administrative Law Judges (ALJs).

Schedule a confidential strategy session today → keep your success story from becoming the next SBA nightmare tale. Contact us at SBA-Attorneys.com for a confidential Case Evaluation.

Sources and links:

SBA employee information for shutdown and furlough

This article is provided for informational purposes only and does not constitute legal advice. Consult a qualified SBA-Attorney for advice regarding your individual situation.

Millions of Dollars in SBA Debts Resolved via Offer in Compromise and Negotiated Repayment Agreements without our Clients filing for Bankruptcy or Facing Home Foreclosure

Millions of Dollars in Treasury Debts Defended Against via AWG Hearings, Treasury Offset Program Resolution, Cross-servicing Disputes, Private Collection Agency Representation, Compromise Offers and Negotiated Repayment Agreements

Our Attorneys are Authorized by the Agency Practice Act to Represent Federal Debtors Nationwide before the SBA, The SBA Office of Hearings and Appeals, the Treasury Department, and the Bureau of Fiscal Service.

Client’s small business obtained an SBA 7(a) loan for $150,000. He and his wife signed personal guarantees and pledged their home as collateral. The SBA loan went into default, the term or maturity date was accelerated and demand for payment of the entire amount claimed was made. The SBA lender’s note gave it the right to adjust the default interest rate from 7.25% to 18% per annum. The business filed for Chapter 11 bankruptcy but was dismissed after 3 years due to its inability to continue with payments under the plan. Clients wanted to file for Chapter 7 bankruptcy, which would have been a mistake as their home had significant equity to repay the SBA loan balance in full as the Trustee would likely seize and sell the home to repay the secured and unsecured creditors. However, the SBA lender opted to pursue the SBA 7(a) Guaranty and subsequently assigned the loan and the right to enforce collection to the SBA. Clients then received the SBA Official 60-Day Notice and hired the Firm to respond to it and negotiate on their behalf. Clients disputed the SBA’s alleged balance of $148,000, as several payments made to the SBA lender during the Chapter 11 reorganization were not accounted for. To challenge the SBA’s claimed debt balance, the Firm Attorneys initiated expedited discovery to obtain government records. SBA records disclosed the true amount owed was about $97,000. Moreover, because the Clients’ home had significant equity, they were not eligible for an Offer in Compromise or an immediate Release of Lien for Consideration, despite being incorrectly advised by non-attorney consulting companies that they were. Instead, our Firm Attorneys recommended a Workout of $97,000 spread over a lengthy term and a waiver of the applicable interest rate making the monthly payment affordable. After back and forth negotiations, SBA approved the Workout proposal, thereby saving the home from imminent foreclosure and reducing the Clients' liability by nearly $81,000 in incorrect principal balance, accrued interest, and statutory collection fees.

Clients obtained an SBA 7(a) loan for their small business in the amount of $298,000. They pledged their primary residence and personal guarantees as direct collateral for the loan. The business failed, the lender was paid the 7(a) guaranty money and the debt was assigned to the SBA. Clients received the Official 60-Day Notice giving them a couple of options to resolve the debt balance directly with the SBA before referral to Treasury's Bureau of Fiscal Service. The risk of referral to Treasury would add nearly $95,000 to the SBA principal loan balance. With the default interest rate at 7.5%, the amount of money to pay toward interest was projected at $198,600. Clients hired the Firm with only 4 days left to respond to the 60-Day due process notice. Because the clients were not eligible for an Offer in Compromise (OIC) due to the significant equity in their home and the SBA lien encumbering it, the Firm Attorneys proposed a Structured Workout to resolve the SBA debt. After back and forth negotiations, the SBA Loan Specialist assigned to the case approved the Workout terms which prevented potential foreclosure of their home, but also saved the clients approximately $294,000 over the agreed-upon Workout term with a waiver of all contractual and statutory administrative fees, collection costs, penalties, and interest.

Clients personally guaranteed an SBA 7(a) loan that was referred to the Department of Treasury for collection. Treasury claimed our clients owed over $220,000 once it added its statutory collection fees and interest. We were able to negotiate a significant reduction of the total claimed amount from $220,000 to $119,000, saving the clients over $100,000 by arguing for a waiver of the statutory 28%-30% administrative fees and costs.

.jpg)