Stop SBA Wage Garnishment: Legal Options to Protect Your Income

Discover legal strategies to stop SBA wage garnishment and protect your earnings. Understand the process and explore actionable options.

We Provide Nationwide Representation of Small Business Owners, Personal Guarantors, and Federal Debtors with More Than $30,000 in Debt before the SBA and Treasury Department's Bureau of Fiscal Service

No Affiliation or Endorsement by any Federal Agency

Millions of Dollars in SBA Debts Resolved via Offer in Compromise and Negotiated Repayment Agreements without our Clients filing for Bankruptcy or Facing Home Foreclosure

Millions of Dollars in Treasury Debts Defended Against via AWG Hearings, Treasury Offset Program Resolution, Cross-servicing Disputes, Private Collection Agency Representation, Compromise Offers and Negotiated Repayment Agreements

Our Attorneys are Authorized by the Agency Practice Act to Represent Federal Debtors Nationwide before the SBA, The SBA Office of Hearings and Appeals, the Treasury Department, and the Bureau of Fiscal Service.

Our firm successfully assisted a client in closing an SBA Disaster Loan tied to a COVID-19 Economic Injury Disaster Loan (EIDL). The borrower obtained an EIDL loan of $153,800, but due to the prolonged economic impact of the COVID-19 pandemic, the business was unable to recover and ultimately closed.

As part of the business closure review and audit, we worked closely with the SBA to negotiate a resolution. The borrower was required to pay only $1,625 to release the remaining collateral, effectively closing the matter without further financial liability for the owner/officer.

This case highlights the importance of strategic negotiations when dealing with SBA settlements, particularly for businesses that have shut down due to unforeseen economic challenges. If you or your business are struggling with SBA loan debt, we focus on SBA Offer in Compromise (SBA OIC) solutions to help settle outstanding obligations efficiently.

Clients personally guaranteed SBA 504 loan balance of $750,000. Clients also pledged the business’s equipment/inventory and their home as additional collateral. Clients had agreed to a voluntary sale of their home to pay down the balance. We intervened and rejected the proposed home sale. Instead, we negotiated an acceptable term repayment agreement and release of lien on the home.

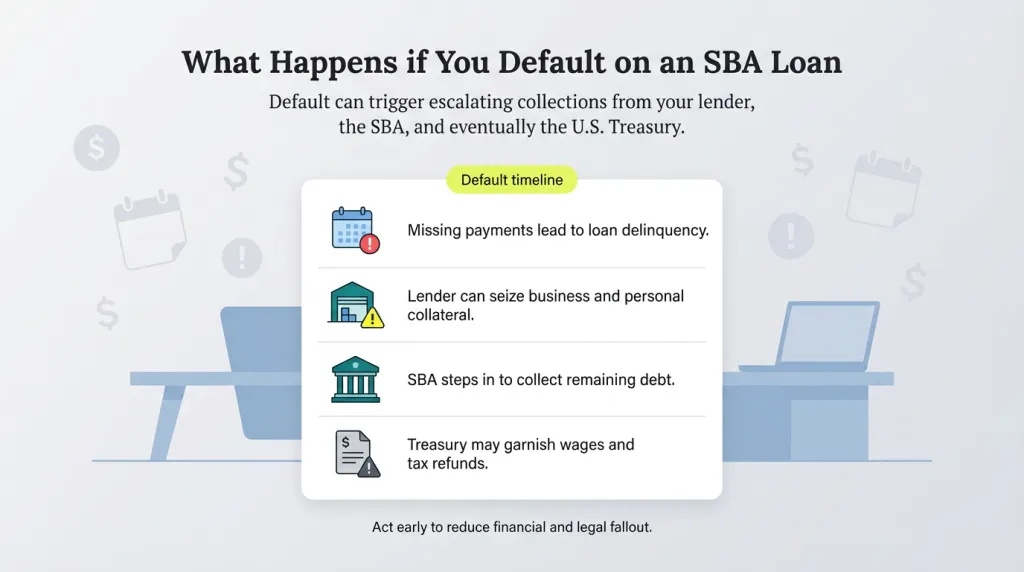

The client personally guaranteed an SBA 7(a) loan for $150,000. His business revenue decreased significantly causing default and an accelerated balance of $143,000. The client received the SBA's Official 60-day notice with the debt scheduled for referral to the Treasury’s Bureau of Fiscal Service for aggressive collection in less than 26 days. We were hired to represent him, respond to the SBA's Official 60-day notice, and prevent enforced collection by the Treasury and the Department of Justice. We successfully negotiated a structured workout with an extended maturity date that included a reduction of the 14% interest rate and removal of substantial collection fees (30% of the loan balance), effectively saving the client over $242,000.

An SBA Loan Modification is a remedial option when the business is still a viable concern, is still generating revenue and due to current circumstances, the old loan terms just do not make financial sense for all parties. A loan modification package is generally presented when it involves a SBA 504 Loan and the collateral or building’s fair market value has decreased significantly such that the loan should probably be modified (i.e. principal and interest payment terms, modification of principal loan balance to reflect current fair market value appraisal of real estate collateral, payment schedule etc.). In this situation, special factors need to be evaluated, appraisals will need to be conducted, and a proposal should be made in order to apply for a loan modification which benefits both parties. Again, the borrower will be required to provide updated business and personal financial information, additional pledged collateral may be requested, and appraisals will be done as part of the modification process. This is not a situation where the borrower or guarantor should engage in this process without qualified representation or consultation. However, if the business feels that it doesn’t need assistance, we recommend that you review applicable SBA SOPs and the Code of Federal Regulations (CFRs) prior to presenting your loan modification application.

An SBA Loan Deferment is a temporary remedial option. If your business is having short term financial difficulty because of a seasonal slump and can reasonably prove through pro forma financial statements to your lender or CDC that a turnaround is around the corner and you need brief relief from paying on the SBA loan, you should consider applying for a deferment. Generally, if you qualify, your bank or CDC, with the SBA’s approval can provide you with either a six (6) month or twelve (12) month reprieve from paying either the principal amount (and allow interest-only payments) or no principal and interest. However, if you consider this option, be advised that you may be asked to reaffirm the loan with personal guarantees or even pledge additional collateral. Needless to say, this is not an option that you should consider without either representation or consultation with a qualified practitioner.

Most SBA loans fall under two categories: 7(a) and 504.In an SBA 7(a) transaction, a loan is secured from a private sector lender and, provided that the lender and borrower have satisfied the requirements of the SBA, if the borrower defaults on the loan, the SBA will reimburse the lender for a percentage on the loan loss (usually 75% or 85%, depending on various factors).In an SBA 504 transaction, typically, a loan is secured from a private sector lender with a first position lien covering up to 50% of the project cost, and a second loan is secured from a private sector lender with a junior lien position covering up to 40% of the project cost, and the borrower makes a contribution of equity equal to at least 10% of the project cost. After the closing of the first and second loans, and provided that the lender and borrower have complied with the requirements of the SBA, a debenture is sold to investors, the proceeds of which pays off the second loan, whereupon the second loan is assigned to a Certified Development Company (“CDC”) and then to the SBA, which provides a 100% guarantee of the debenture.The existence of the SBA’s guarantee in each of these transactions is an inducement for the lender to make a loan on terms it would otherwise not make. However, the SBA guarantee does not allow the lender to disregard standard commercial underwriting principles such as collateral and personal guarantees. The SBA guarantee does allow the lender to loan more money, extend longer terms, and approve loans to less mature businesses than it otherwise would.The SBA’s purpose under these financing programs is to help businesses gain more access to capital, thereby creating jobs and expanding the tax base. Pursuant to the Small Business Jobs Act of 2010 (“2010 Act”), the maximum SBA guarantee to the lender on a 7(a) loan was increased to $5,000,000; and on a 504 Loan, the maximum debenture amount was increased to $5,000,000.

While the SBA prefers a cash settlement offer (i.e., lump sum payment or cash compromise) with an SBA OIC Package, a monthly installment payment plan not to exceed 5 years or 60 months (term compromise) may also be considered if necessary. If a term compromise is desired, the SBA may also require a lien on any worthwhile collateral that may be available to secure the agreed upon balance due.

Creditors' committees commonly occur in traditional Chapter 11 cases, but they need a cause in Subchapter V cases.

Subchapter V trustees' primary function is to create a standard plan with the debtor and creditor. They do have the authority to audit the debtor's finances, but their primary purpose is mediation.

The reason for this is Congress sees impartial third-parties' increasing the likelihood of a sound resolution among the debtor and its creditors. Unbiased third parties are especially useful for small businesses whose creditors are tentative as a result of COVID.

.jpg)

.jpeg)

.jpg)